NM APARTMENT

1 9 8 9

REPORT

1 9 9 8

"Market Forecast '99 - Occupancy"

Originally appeared inNM Apartment Report

Albuquerque

Once the hottest market in the Southwest, Albuquerques contiuned declining occupancy rates, fueled by the overwhelming presence of manufactured housing, four years of increasing rent levels, and the return of affordable single family residences has set the occupancy rates on a downhill slide since 1995.

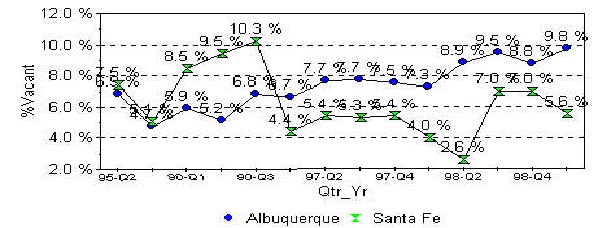

Current absorption studies indicate that a positive absorption exists, prior to calculating leakages to other markets like manufactured housing. The chart (below) demonstrates the last four years of physical occupancy rates for the greater metro area. Once incentives and rent concessions are factored in, (if half of the apartment communities offer 1 month free) - then that decreases occupancy by 100%/12months - 8.33% per month x 1/2 = 4.167% thus decreasing true occupancy to the mid 80% range.

Sub-market Reports:

The main engine of production for new units in the early 1990s, The NE Heights, has strengthened in the last two years, end in 1999 under 10% after a 1997 high at 12%.

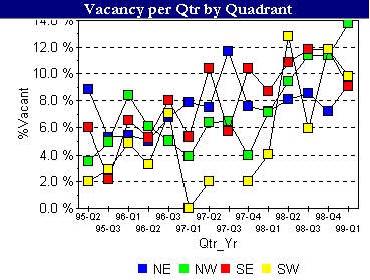

The NW Heights, once home to 10% of the total supply of Albuquerque apartments, has witnessed a growth in new construction in excess of 25% of its own supply, in part increasing vacany rates to the 14% range today.

The triangle shaped SE Heights that encompasses an area as slim as three blocks deep on the far east to three miles deep near the airport, witnessed a lack of demand as their tenants took advantage of the amenties, new features, and favorable rents offered in the new communities located in the NW and NE. The last quarter has witnessed a reverse of this trend, indicating the potential desire by residents to live closer to major employment centers (University, Lovelace/VA, Sandia Labs, Airport, Downtown, etc.)

The largest potential quadrant (in land mass), SW, also contains the smallest number of units (less than 2,000). The recent supply of new rental and ownership housing has dragged the once stable occupancy rate to record highs. Although long term residential growth will have to occur in this location, besides the downtown core, do not expect new construction in this area for a couple of years.

Vacancy rate by Grade

A+ - although this segment of the market appears to have undergone the most dramatic swings in vacancy rates, the highs in 1995 and 1998 reflect the addition of the Pinnacle at High Desert/High Estates and High Resort coming on line. The lack of quality sites (except for one potential), will most likely lead to no new construction in this segment.

A - The A product has also shown decreasing vacancy rates as new product reaches stabilization points.

B+/B - These two markets paralled each other until 1998, when the B+ properties pulled down their vacancy rates by decreasing rents or increasing concessions, encouraging B residents to convert to B+ communities.

C - Often scorned by institutional investors, the C market represents older properties in established neighborhoods often co-located near major employment centers or the University of New Mexico. This market segmentation has maintained below average vacancy rates and has continually beaten the market. Another key factor in this arena, most of the communities in this range offer larger units with the landlord paying for all/most utilities.

D/F - Although the D market was once at 2%, the recent influx of manufactured housing, inexpensive single family residential, low interest rates, and the conversion of some of these communities in HUDs Mark-to-Market program has demonstrated that these communities, even rehabbed may not have what it takes to be competitive with the market, ending 1998 in excess of 12%, representing the single largest increase in vacancy factor of any of the grades.

El Paso/Las Cruces

Often overlooked by institutional investors, both of these markets have demonstrated an amazing resilience during a storm of new construction. The similarity between these two markets reflects their close proximity, and a strong collegiate housing presence in each market. Although several large University Housing Developers have targeted these makets, new construction is anticipated to be minimal, encouraging even lower vacancy rates, and potential modest rental increases.

Article by

by Todd Clarke CCIM (www.nmcomreal.com/nmcomreal)

p a g e

o n e