NM APARTMENT

1 9 8 9

REPORT

1 9 9 8

"Market Forecast '99 - Population Forecast"

Originally appeared inNM Apartment Report

National Trends

The following summary is abbreviated from the Harvard Reports,State of the Nations Housing 1998

Now in its eighth year of sustained growth, the U.S. economy has brought unprecedented strength to housing production and sales. Spurred by strong employment growth, low mortgage interest rates, and new more flexible financing options, national homeownership rates have reached an all time high. The gains in homeownership are broadly based, with young adults making up much of the ground they lost during the 1980s, and minority and moderate-income households purchasing homes in record numbers.

Although growing numbers of families are gaining access to the wealth-building opportunity of homeownership, the number of households without access to decent and affordable housing is also growing. With lower inflation, adjusted earnings than their counterparts 15 years ago, today's 25 to 34 year-olds with only a high school education are falling further and further behind in their ability to progress up the housing ladder. Meanwhile, affordability is by far the most pressing problem for the 8.6 million renter and 5.6 million owner households with extremely low incomes.

For those households with severe payment burdens, no relief is in sight. In fact, the imbalance between the supply of and demand for rental units affordable to the nations lowest-income households is worsening. Even after a protracted period of rent deflation when about 260,000 rental units filtered down to the low-cost stock, the affordable inventory has continued to shrink because of losses to abandonment and demolition. On top of these pressures, the number of net new commitments for rental subsidies remains at historically low levels.

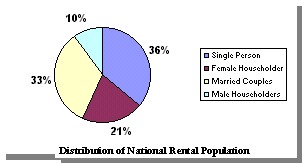

The above chart indicates the breakdown of apartment renters on a national level. As you can see 90% of the national rental population is family oriented, which are natural targets to those offering the American dream - homeownership. Since housing costs have increased exponentially over the last 15 years, single family residential ownership is even further out of reach for most renters.

The following factors are also driving many renters to convert to manufactured housing:

Impact of Manufactured Housing - Common Trends Nationally

� Increased service-sector job creation in southeast and southwest regions (traditionally strong areas for manufactured housing)

� Aging baby boomer population

� Generation "X" population moving into first time home-buying market

� Substantial cost savings (20-50%) versus site built housing

� Greater availability of financing including longer loan terms

� Improved construction quality and appearance

� Population shift towards suburban and rural areas (traditionally strong areas for manufactured housing)

� Increased ability to site homes in subdivisions using experienced developers

� Growing share of the single family housing market (32% in 1996)

� Rebirth of Texas economy

� Increased housing formations

� Housing, in general, losing it's investment appeal (consumers satisfied with more modest housing)

Albuquerque is listed as the 12th fastest growing city in the country for the period 1940-1990 - with a growth from 103,534 residents to 589.131, representing a 469% increase. Additionally, Valencia and Sandoval counties are projected to be the 17th and 29th fastest growing counties (out of 841) in the country.

Limits on Growth

After the construction boom in the mid 1980s, supply of new apartment units in the metro area slowed to as little as sixty-six new units in 1993. The lack of construction allowed apartment owners and managers a rare opportunity to increase rents from $.45/sf in 1989 to $.74/sf in 1995. Since that time, rents have stabilized in the $.72/sf to $.73/sf range.

Although Albuquerque is perceived to have an abundance of land, it is corralled by Indian Reservations, Government Reservations, and National Parks on all four boundaries. This boxing in of Albuquerques growth has contributed to an artificial appreciation for land prices as compared to other southwestern cities.

For the first time since the mid 1980s, rental increases in the early 1990s allowed developers to consider new multi-family development based on current land prices. A majority of the remaining infill parcels in the NE Heights were purchased and developed as A or A+ communities totaling some 3,335 units. Most of these units were funded by REITs or Pension Funds, who focused their efforts on quality long term projects. As these new communities came online, the average rental monthly absorption rate was 20 units per community. Those communities that possessed excellent management staff were able to lease up to 45 units per month, while those lacking in management leased as little as 10 units per month. Fortunately, the lack of available multi-family land has slowed the development of A communities. What little land is still available is being actively developed as B communities, most with a tax credit or bond enhancement program.

According to absorption figures collected for the last few years, Albuquerque has enjoyed an average positive absorption of apartment units of 1,200 units per year. After taking into account leakage to other product types either single family residential (with its incredibly low interest rates) or manufactured housing (with its incredibly low prices), annual apartment absorption is decreasing to approximately 250 units per year. Currently there is only enough multi-family land to support less than 1,500 new units.

Demand

Tracking the supply side of absorption is relatively easy as compared to the demand side. The 1990 census figures indicate that on average there are 2.65 individuals per residence and that approximately 35% of residential occupants rent versus purchasing.

As the above table indicates, the Albuquerque MSA has undergone phenomenal job growth, and continues to maintain a below average unemployment rate. Unfortunately, the usually commensurate population growth has not been witnessed. Local economists question the accuracy of these population figures, but until another reliable source is validated, these are the best possible numbers for this study.

Other variables:

Rent Levels: Given the significant rental increases that Albuquerque has witnessed over the last few years, new construction is not as large of a competitor as the lack of affordable housing. With an average unit size of 850 square feet, and an average monthly rent per square foot of $.72, the average monthly rent for the city is $612. Adding another $88 for utilities in monthly charges raises the typical familys housing cost to $700 per month. Annualizing this yields a value of $8,400. To qualify for most apartments, a tenant can only utilize 33% of their annual income for housing needs. Multiplying $8,400 x 3 yields a minimum household income of $25,200. In 1990, this same calculation yielded a minimum household income of $15,300. To look at this another way, personal income needed to increase by $1,428 per year each year for the last seven years to maintain the same standard of living.

Big I renovation: Currently the State Highway Department is reviewing several different plans on how to best renovate the interchange where New Mexicos two largest interstates (I-25/I-40 intersect. The Big Ihas not undergone a significant renovation since its construction in the mid 1960s. Originally designed to carry interstate traffic (not local), its current design of scrunching four lane highway traffic down to one or two lanes is grossly inefficient. The current traffic load of 150,000+ cars per day subjects the interchange to fatigue and use for which it was never intended. Unlike the balance of the city that is laid out on a grid system, the area surrounding the interchange consists of meandering sub-arterial streets that carry less than 15,000 cars per day on average. One of the plans involves the development of frontage roads to carry cars through the interchange until its completion. In any event, the renovation of the Big I, which is scheduled to begin in 1999, will wreak havoc on those who live in the Far NE Heights or Tanoan neighborhoods.

KAFB Current market demand for housing from KAFB is 3,000 units (rental & ownership) - this is expected to decrease over the next 5 years to 2,800 due to force reductions and outsourcing, 1,400 of whom are expected to purchase homes, leaving the balance to seek rental housing.

Currently KAFB has 1,890 housing units - the future plans include: keep 211 units, construct 953 new units in a 5 year time span, demolish 1,046 within six years, release the balance of 633 units to the general market. New rental units to provide 1,175 square foot 2 bedroom units, 1,490-1,610 square foot 3 bedroom units, and 1,675-2,600 square foot 4 bedroom units. Current timeline calls for July 1, 1999 RFP, September 1, 1999 response, January 2000 selection followed by execution of contract and beginning of project.

-KAFB - Housing Privatization update 1/13/99

National Aging Trends

At the onset of this century, a mere four percent of the U.S. population lived beyond sixty-five years of age. Life expectancy in 1900 was 49.2 years. Today it is nearly 75 years. Aging of the American population is not a new phenomenon. Our population has been growing older since about 1800. In the year 1800, 50 percent of the population was under the age of 16 and very few people lived to see age 60. Today, some 30% of our population is 50 years and older.

The above graph is a population forecast based on the 1990 census forecast for the Albuquerque MSA, segregated by age group. The data indicates that the fastest growing segment of the population is the 50-59 age group, followed by the 60-69 and older age groups.

Article by

by Todd Clarke CCIM (www.nmcomreal.com/nmcomreal)

p a g e

o n e