NM APARTMENT

1 9 8 9

REPORT

1 9 9 8

"Grubb & Ellis - Capital Markets Update"

Originally appeared inNew Mexico Apartment Fax

Compiled by Grubb & Ellis

Section I

Capital Market Overview

Late in 1998, the Federal Reserve implemented three interest rate cuts to combat a credit freeze caused by Russias default on its bond debt, financial turmoil in Asia and Latin America, and the collapse of a major hedge fund. There was a widespread belief at the time that these problems would, at best, slow U.S. economic growth and, at worst, drag the U.S. into a global recession. Commercial property values, it was feared, would decline by up to 20%, and investment activity would slow to a crawl until values stabilized and liquidity returned.

Not only did the rate cuts restore liquidity to the capital markets, they helped boost the fourth quarter Gross Domestic Product to an annualized rate of 6.0%, the second highest quarterly increase since 1984. First quarter growth also has been robust at 4.5%, well above the 3.9% average in 1997 and 1998. Property investment activity, which fell sharply late last year, picked up again in the first quarter, and there has been surprisingly little impact on property prices. In fact, the rate cuts appear to have worked so well that inflation, not recession, is now the main concern of policymakers. Consumer prices, adjusted for seasonal differences, jumped sharply by 0.7% in April, prompting the Federal Reserve to announce a bias toward tightening interest rates, most likely later this year. The year-over-year inflation rate was 2.3% in April, up from 1.4% early in 1998.

Last years reductions in the Federal Funds Rate induced a sharp decline in other interest rate indexes. Ten-year Treasuries fell from 5.52% on July 29th, 1998 to a low of 4.16% on October 5th and have since rebounded to 5.62% as of May 14th, 1999. Thirty-year Treasuries fell from 5.77% on July 29th to 4.70% on October 5thand are currently yielding 5.92% as of May 14th. Rates appear to be heading higher as private lenders react to Mr. Greenspans bias toward tighter credit.

The CMBS market (commercial mortgage backed securities) suffered a direct hit during the capital freeze late last year. Investors stampeded into high-quality debt instruments, driving rates for Treasuries to their nadir in early October, and stampeded out of CMBS and other debt instruments perceived as risky. This was perhaps a watershed event showing investors that real estate was no longer the parochial business it was in the 1980s. Spreads for AAA-rated tranches, which hit a low of 63 bp above Treasuries in mid-1997, ballooned to 165 bp in September of 1998 before returning to around 90 bp as of mid-May 1999. BBB-rated tranches hit a low of 90 basis points in mid-1997, a high of 265 basis points in September of 1998 and are currently at 205 basis points. The steady narrowing in the spreads since last fall indicates that CMBS is once again in demand from investors and remains a viable funding source for the commercial real estate industry.

Equity Capital Sources

Commercial property investors can be divided into five categories: REITs (real estate investment trusts), institutional, opportunistic, private and offshore. However, the lines between them are blurring as different categories of investors initiate partnerships and commingled funds, and as the real estate market evolves, making particular investment strategies more or less attractive.

REIT capitalization currently stands at approximately $144 billion, up nearly 17-fold from the beginning of the decade. In recent years, REITs have been the largest acquirers of property nationwide. REITs earned robust returns for their investors from 1991 through 1993 and again from 1995 through 1997, and their healthy stock prices translated into a low cost of capital through initial and secondary stock offerings, allowing REITs to compete aggressively for acquisitions.

REITs suffered a setback in 1998 as their share prices declined sharply on fears of overbuilding, making it difficult for them to tap the capital markets and maintain their pace of acquisitions. The good news is that REIT share prices jumped 9.4% in April of this year after Warren Buffet announced his recent investment in a REIT and his belief that REITs are undervalued. The April jump could be the first sign that REITs are regaining favor with investors, which could reopen their access to the capital markets later this year. Nevertheless, equity REIT prices remain 12% below their average share price on January 1, 1998, and mortgage REITs are off by 27%. Other potential sources of funding for REITs include increased borrowing and partnering with other investors to pursue strategic acquisition and development projects. Merger and acquisition activity in the REIT industry is expected to increase as well. During 1999, REITs will look for ways to increase FFO through prudent asset management, property management and internal operating efficiencies, rather than through another big cycle of acquisitions.

Institutional investors include pension funds and their advisors, life insurance companies, banks and savings associations. Pension funds and advisors hold approximately $121 billion of equity real estate on their books; insurance companies account for $43 billion, while banks and savings associations hold a relatively small $4.1 billion of total equity. Institutional investors were big net sellers of real estate during 1998. With REITs sidelined by low share prices late in the year, however, institutional investors, led by pension funds and advisors, returned to the market, taking advantage of subdued competition and greater negotiating leverage. Because many of the major public pension funds are dramatically under-invested in real estate, they are expected to continue their acquisitions during 1999.

Opportunistic Investors include commingled pools of capital backed by institutional investors, notably pension funds and Wall Street investment banks. The funds have different investment objectives, return parameters and holding periods but share a willingness to accept greater risk in search of greater returns. Their investments tend to be in properties with higher vacancies, greater rollover risks and mixed tenant credit profiles. These funds, totaling approximately 50 in number, are sponsored by a variety of entities, including well known names such as AEW, Apollo, Blackstone, Beacon Capital Partners, Lazard Freres, Walton Street and Whitehall (Goldman Sachs). In the current mature phase of the real estate cycle, opportunities for value-added investing are limited, and opportunity funds may pursue strategies and return objectives more closely associated with institutional investors.

Private investors include developers, private operating companies, limited liability companies, partnerships and high net worth individuals. Private investors are estimated to account for slightly more than half the total combined value of all U.S. commercial real estate debt and equity. Private investors are tapping opportunity funds and institutional capital to co-invest and pursue larger opportunities. In 1997 and the first half of 1998, many private investors were leveraged by the CMBS market, a source of capital which is returning cautiously. Private investors that have sold properties to REITs or refinanced their portfolios are actively re-investing the proceeds.

Offshore capital currently active in the U.S. comes primarily from Canada, Europe, the Middle East and Asia. Foreign investors account for approximately $37 billion of U.S. real estate equity investment. Aggressive offshore investors have been responsible for several of the largest deals in 1999. These investors are most comfortable with high profile properties in primary markets, particularly CBD office properties in major East and West Coast cities.

Capital Flows

Capital flows into real estate during 1998 totaled an estimated $141 billion according to Goldman Sachs. The company forecasts that capital flows this year will total approximately $100 billion. The decline is due to the fact that REITs will be far less aggressive in pursuing acquisitions during 1999 than they were during the first half of 1998.

The forced departure of REITs created an opening for other investors to jump into the acquisitions arena, and many have done so. But the number of investment deals is still down from the supercharged levels of 1997 and early 1998, which now appear to be an abberation. Deals tracked in the database maintained by Institutional Real Estate, Inc., totaled $16.6 billion in the first quarter of 1999. This was well above the $10.1 billion of deals announced in the fourth quarter of 1998 but considerably below the 1998 second quarter deal volume of $25.4 billion.

During the first quarter of 1998, REITs accounted for 69% of all announced commercial real estate acquisitions. Private investors accounted for 11%, while no other group accounted for more than 8% of the total. REITs were able to dominate bidding in 1997 and the first half of 1998 thanks to their rich share prices and low cost of capital. Many non-REIT investors were priced out of the market and chose to move to the sidelines until conditions changed.

And change they did as REIT share prices dropped slowly in the first half of 1998 and then more steeply in the second half. By the first quarter of 1999, REITs accounted for 28% of announced acquisitions and were eclipsed by the 30% share of private investors. Opportunistic investors accounted for 18% of the total, while institutional and offshore investors each accounted for 12%. The market share numbers from the first quarter of 1999 indicate a more level playing field where no single investor group is dominating the market. They also show that REITs, still the second most active investor group, are far from down and out. The recent rise in their share prices coupled with the REIT Modernization Legislation currently pending in Congress are evidence that REITs will remain strong and aggressive players in the real estate investment market.

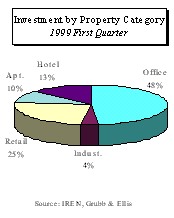

During the first quarter of 1999, office properties accounted for nearly half the value of all announced investment acquisitions, followed by retail properties with a 25% share, hotels with 13%, apartments with 10% and industrial properties with 5% of the total. These shares are similar to 1998 except for a slight elevation in the share of investment dollars flowing to office properties offset by a decline in capital flows to apartment properties. The relatively constant proportion of capital flows to the five major property categories indicates that investor preferences have changed little during the past year. There has been some talk of overbuilding in all the property types, particularly budget and limited service hotels, but also apartment, industrial, retail power centers and suburban office properties in selected markets. But generally all five property markets remain in balance and are attracting a steady flow of investment capital. In submarkets where overbuilding has occurred, developers and lenders generally have stepped back to let demand catch up with supply.

In summary, 1999 has ushered in a balanced, steady investment market. The economy remains strong, liquidity is plentiful, and there are many buyers and sellers in the market creating opportunities for all types of investors and all property categories. Following the steep run-up in prices during the past three years, there are fewer opportunities for home run and value-added acquisitions. The only flashing yellow light is the potential for higher interest rates later this year.

Section II

Multi-family Market Trends

Capital market trends in the multi-family property sector mirror those in the overall capital markets. The volume of multi-family deals announced in the first quarter totaled $1.6 billion, up from the $1.4 billion announced in the fourth quarter but well below the $3.9 billion announced in the first quarter of 1998. During the first two quarters of 1998, REITs played a larger role in the multi-family acquisitions market than in other property categories. In the first quarter of 1998, REITs accounted for 84% of the value of announced multi-family acquisitions compared to 69% of the total volume of acquisitions in all property categories. The ratio held in the second quarter as well, with REITs accounting for 75% of multi-family acquisitions versus 64% of all property acquisitions. The greater role played by REITs in the multi-family sector could explain why multi-family property sales in the first quarter of this year failed to bounce back quite as strongly as other property categories.

Prices for multi-family properties showed surprisingly little change during the past year considering the capital markets turmoil. Data provided by Institutional Real Estate indicate that the average price per unit in deals announced in the third quarter of 1998 dropped by 6% from the second quarter. But prices per unit in the fourth quarter of 1998 and first quarter of 1999 bounced back into the low-$60,000 range, equivalent to an increase of 5% in the fourth quarter (relative to the previous quarter) and 1% in the first quarter of 1999. The third quarter decline in the price per unit could have been the result of softer market conditions, but more likely it was a one-quarter blip in the data resulting from the particular mix of property deals announced during that quarter.

The blip explanation seems more plausible in light of cap rate data provided in the Korpacz Real Estate Investor Survey. Korpacz data show the multi-family cap rate reaching a cyclical low of 8.76% in the third quarter of 1998 and then increasing slightly to 8.77% in the fourth quarter and 8.83% in the first quarter of 1999. The Korpacz data show the cap rate reaching a low point during the same quarter that the data from Institutional Real Estate show a decline in the average multi-family property price, a relationship that seems contradictory. The explanation could be that the Korpacz third quarter cap rate was derived from surveys completed early in the quarter when REITs were still bidding actively for properties and lenders were still very aggressive. From the first quarter of 1998 to the third quarter of 1998, the multi-family cap rate fell by 12 bp, and from the third quarter of 1998 to the first quarter of 1999, it rose by seven bp. Overall, the changes were modest, concurring with the IRE price-per-unit data that multi-family prices have shown relatively little change during the past few quarters. This suggests that the slowdown in the property investment market during the second half of 1998 arrested the rise in multi-family property prices rather than causing prices to actually decline.

Multi-family Space Market

Multi-family space market conditions remain very strong as a result of the robust economy coupled with development activity that has remained in line with demand for the past few years. Data from the U.S. Census Bureau indicate that the nations rental housing vacancy rate has been relatively stable this decade, rarely venturing beyond the range of 7% to 8%. The first quarter 1999 vacancy rate of 8.2% is slightly above this range. Data from M/PF Research show that the vacancy rate for its sample of institutional-grade (Class A) multi-family properties has fallen gradually since the early 1990s and stands at 5.1% in the fourth quarter of 1998. The gradual decline in the M/PF Class A vacancy index coupled with the stability of the Census Bureau vacancy index for all rental properties suggests that newer, Class A properties have been leasing well, but not at the expense of the overall universe of properties.

Rental rate growth in the M/PF sample of institutional grade properties has been very healthy. The year-over-year same-store rent growth was a strong 4.9% in the fourth quarter of 1998, the largest increase in several quarters.

Multi-family permit activity has risen gradually since the early 1990s in line with demand. Permit activity for April 1999 fell to a seasonally adjusted annual rate of 296,000 units, the lowest level in nearly two years. While it is too early to state that the reduced permit activity is more than a one-month blip, the trend bares watching because it could indicate a note of caution on the part of developers and lenders.

Investment returns for both multi-family REITs and multi-family property investments held by institutions have performed well relative to other property categories. According to the National Association of Real Estate Investment Trusts (NAREIT), apartment REITs have returned 8.23% so far in 1999 versus 2.92% for all REITs. The National Council of Real Estate Investment Fiduciaries (NACREIF) reports that apartment investments held by pension funds and their advisors returned 2.66% in the first quarter of 1999 compared to 2.53% for all property types.

In summary, both the multi-family capital and space markets are healthy. As in the capital markets overall, the only danger for the apartment market at the present time appears to be the potential for higher interest rates later this year. But even higher interest rates will have a silver lining for this property category because fewer households will qualify for homeownership as mortgage rates rise, translating into a larger overall pool of renter households.

Article by

by Todd Clarke CCIM (www.nmcomreal.com/nmcomreal)

p a g e

o n e